Top Crypto-Friendly Banks in Latin America for 2026: Risks, Reviews & Regulations

An analytical 2026 review of crypto-friendly banking in Latin America: jurisdiction-driven differences, compliance behavior, fintech intermediaries, and user experiences across Brazil, Mexico, Argentina, Colombia, and Panama

Have you ever wondered why crypto-friendly banks have become such a critical topic in Latin America? The answer lies in a different set of drivers than in Europe: persistent currency volatility, capital controls in certain countries, rapid fintech adoption, and a growing need for reliable fiat-crypto access outside traditional banking limitations. In Mexico, Argentina, Brazil, Colombia, and Panama, crypto is no longer just a guess; it's a useful financial tool.

The crypto-banking scene in Latin America is very different from that in Europe, where regulations are becoming more similar. Some places have established rules and licensed middlemen, while others work in less formal or more necessary contexts. This diversity makes banks operate differently: certain banks may allow, limit, or monitor crypto transactions based on the bank, the country, and even the magnitude of the transaction.

This guide is a full, honest, and analytical review of crypto-friendly banking in Latin America. You will see real user experiences, region-specific comparisons, and practical guidance on how to assess bank accounts to avoid common issues such as account freezes, AML flags, or sudden policy shifts. By the end, you will have a clearer understanding of which approaches work in the region today – and which ones are most likely to cause problems tomorrow.

Summary (2026)

By 2026, crypto banking in Latin America has become practical and mostly predictable, though rarely seamless. Banks no longer treat crypto as exotic, but direct support remains limited, and access often looks different from what marketing suggests.

In practice, outcomes depend less on the bank and more on jurisdiction and transaction behavior. In Brazil and Mexico, mature payment systems allow relatively smooth everyday transfers. In Argentina, Colombia, and Panama, the same actions usually require tighter documentation and a higher tolerance for manual compliance checks.

A Realistic Breakdown of Markets and Risks

Understanding crypto banking in 2026 starts with geography. Regulatory tolerance, compliance culture, and enforcement vary sharply across Latin America [14], making bank behavior highly jurisdiction-dependent.

The Regional Map at a Glance (2025)

| Region | Friendliness Level | Key Characteristic | Primary Risk | Top Advice |

|---|---|---|---|---|

| Brazil | Medium–High (Structured) | Clear crypto regulation, CBDC (Drex) pilot, strong fintech sector | Enhanced AML reviews, reporting obligations | Use regulated banks and licensed exchanges; keep transaction history |

| Mexico | Medium (Selective) | Strong fintech law, crypto allowed via intermediaries | Banks refuse direct crypto exposure | Operate via SPEI-supported platforms; avoid direct exchange labeling |

| Argentina | High (Necessity-driven) | Crypto widely used as inflation hedge | Capital controls, sudden policy shifts | Diversify banks and keep balances low |

| Colombia | Medium (Pilot-based) | Sandbox programs for crypto exchanges | Limited long-term guarantees | Use sandbox-approved partners only |

| Panama | Medium (Flexible but opaque) | Dollarized economy, banking flexibility | Weak regulatory clarity | Maintain full documentation; avoid large spikes |

With this context established, we can move from regional patterns to how they play out in specific markets.

Crypto-Friendly Banks & Fintechs in Latin America: Operational Matrix (2026)

To help you evaluate faster, here's a bank matrix summarizing practical advantages and challenges across Latin American markets, based on active user experience through 2025, fintech adoption trends, and regulatory positioning heading into 2026.

| Bank / Fintech | Region | Strengths | Common Issues | Crypto-Friendliness |

|---|---|---|---|---|

| Nubank | Brazil | Large retail base, PIX transfers, fintech integrations | No direct crypto banking; AML reviews on volume spikes | 🟡 Moderate |

| Banco Inter | Brazil | Fast PIX payments, access to crypto ETFs | Transaction reviews for exchange-related flows | 🟡 Moderate |

| BTG Pactual | Brazil | Institutional-grade crypto services, regulated infrastructure | Not designed for retail users | 🟢 Smooth |

| Bitso (Fintech) | Mexico | SPEI integration, licensed exchange rails, strong liquidity | Reliant on partner banks for fiat rails | 🟢 Smooth |

| BBVA Mexico | Mexico | Strong compliance framework, large-scale stability | Conservative handling of crypto-linked transfers | 🟡 Moderate |

| Santander Argentina | Argentina | Practical tolerance toward local crypto usage | FX controls, regulatory volatility | 🟡 Moderate |

| Banco Galicia | Argentina | Works with local crypto platforms | Sudden compliance checks possible | 🟡 Moderate |

| Bancolombia | Colombia | Sandbox-backed crypto pilots with exchanges | Limited scope, capped volumes | 🟡 Moderate |

| Banco General | Panama | USD accounts, regional banking flexibility | Manual compliance and transaction reviews | 🟡 Moderate |

| Towerbank | Panama | Reputation for crypto tolerance, USD rails | Strict onboarding, enhanced documentation | 🟢 Smooth |

Color guide: 🟢 = smooth, 🟡 = cautious, 🔴 = risky.

The matrix is designed for quick comparison: it summarizes operational strengths and friction points across banks and fintechs, rather than formal ‘crypto support’ claims.

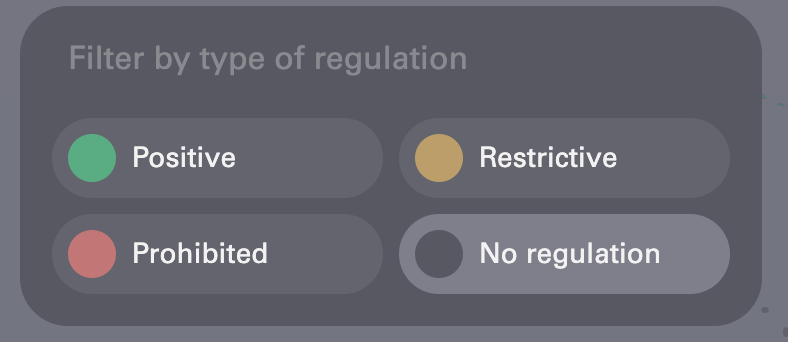

To present a visual picture of the disparities in crypto-friendly banking throughout Latin American areas in 2026, we use the D&A CryptoMap, which depicts the regulatory and operational friendliness of crypto payments. Keep in mind that these are general tendencies; real bank-by-bank conduct may vary and change swiftly due to internal policy and regulatory revisions.

Overview of crypto regulation and banking access across Latin America in 2026.

Overview of crypto regulation and banking access across Latin America in 2026.

According to D&A CryptoMap [14], this visual depiction gives readers a clear picture of regional patterns in Latin America and helps them interpret variances in crypto banking practices.

On the map, green denotes governments that are generally supportive of cryptocurrency payments, with banks and fintechs expected to enable crypto-fiat activities with minimum limitations. Yellow indicates regions with a cautious or mixed attitude, which means that certain banks may impose constraints, do additional AML checks, or rely on fintech intermediaries. Red indicates restrictive regions, where crypto payments are limited or subject to stringent compliance inspection, and users may face account freezes or manual reviews.

While our detailed review focuses on the five key Latin American markets – Brazil, Mexico, Argentina, Colombia, and Panama – other countries like Guatemala are beginning to show early signs of regulated crypto access. Users there can leverage regulated intermediaries, though documentation and cautious transaction practices remain essential [14].

Now, we are going to start with Brazil, the most active crypto hub in the region, and examine the specific banks and fintechs shaping the landscape.

Brazil: The Growing Crypto Hub of Latin America

Brazil has been one of the most active places in Latin America for banks that accept cryptocurrency. The country's fintech regulations are clear, there is a functioning CBDC pilot (Drex) [2], and PIX [1] has a developed payments infrastructure. Banks follow AML and transaction monitoring rules very closely, although they usually let people use crypto through middlemen and fintech partnerships.

In operational terms, Brazil’s crypto-friendly reputation is built less on explicit crypto support and more on predictable payment infrastructure and strict compliance logic at the bank level. In practice, Brazilian banks allow crypto-related activity primarily through intermediaries and fintech integrations while closely monitoring transaction patterns. What matters most is not whether crypto is involved, but how consistently and transparently activity aligns with a normal financial profile.

Nubank [7] and Banco Inter [8] are examples of neobanks that are easy to use and accessible. They enable PIX-based transfers, multi-currency accounts, and indirect access to crypto services. Their biggest problem is that consumers can't directly hold or trade crypto in their bank accounts, and big or frequent transactions may cause AML reviews or temporary holds.

Nubank makes it easy to do ordinary banking on your phone, with quick PIX payments and connections to other financial apps. Transfers related to crypto may be checked when quantities rise, which might cause delays or require paperwork, even though they are easy for retail customers.

Banco Inter lets you make quick PIX payments and buy crypto ETFs through partners. It works well for everyday tasks, although flows relating to exchanges are closely watched, and larger transfers may be subject to surprise compliance checks.

In contrast, BTG Pactual [9] mostly works with institutional clients. It has regulated, institutional-grade crypto services that work with professional trading platforms, but regular people usually can't use them directly. BTG Pactual offers smoother transaction rails with fewer disruptions for businesses or wealthy people who want dependable crypto operations.

These patterns are reflected in the operational matrix above, where most institutions fall into the “moderate” category due to conditional access and compliance-driven reviews.

Mexico: Regulated Crypto Access via Fintech Partners

Mexico stands out for its regulated yet cautious approach to crypto-related banking. The country does not have a large ecosystem of consumer-focused “crypto neobanks” like those found in Europe or Brazil, instead relying on fintech platforms and licensed exchanges to facilitate crypto access under regulatory supervision [3].

In operational terms, crypto access in Mexico is defined by regulatory routing rather than bank-level enablement. Mexican banks generally avoid direct cryptocurrency exposure and instead rely on licensed fintech platforms to intermediate crypto-fiat flows.

Transactions that move through regulated rails with clear counterparties and documentation tend to process predictably, while activity that appears direct, unusually large, or behaviorally inconsistent is more likely to trigger enhanced due diligence. In practice, consistency of transaction patterns and alignment with a user’s declared financial profile matter more than transaction size alone.

Bitso [10], Mexico’s largest licensed crypto platform, integrates with SPEI for fiat transfers and provides regulated trading and custody services. As a fintech intermediary, Bitso enables both retail and institutional users to operate within clearly defined compliance frameworks, making it one of the most reliable crypto-fiat access points in the country.

BBVA Mexico [11], a major traditional bank, offers strong compliance frameworks but treats crypto-linked transactions conservatively. Transfers to licensed exchanges are allowed, yet unusual or high-value operations may require additional documentation on sources of funds (SOF) and sources of wealth (SOW), and some transfers could be delayed for review.

As a result, users in Mexico tend to rely on fintech platforms such as Bitso for operational flexibility, while banks remain focused on compliant fiat account management.

The Argentine market contrasts with Mexico, where crypto access is structured primarily through regulated fintech intermediaries.

Argentina: Maneuvering Cryptocurrency Amid Policy Volatility

Argentina offers a distinctive landscape for crypto banking, influenced by persistent inflation, capital controls, and abrupt regulatory changes imposed by monetary authorities [4]. Cryptocurrency is widely used as a hedge against peso depreciation; however, financial institutions remain cautious and closely monitor crypto-linked transactions.

In operational terms, crypto banking in Argentina is driven more by economic necessity than regulatory clarity. Banks generally tolerate indirect crypto activity when transaction sizes remain modest, patterns are stable, and documentation aligns with declared income. However, foreign exchange controls and shifting regulatory signals mean that even compliant activity can move from routine processing to manual review with little notice. Predictability depends less on the bank itself and more on timing, volumes, and alignment with current FX and capital control rules.

Santander Argentina [16] and Banco Galicia [17] are examples of banks that cooperate with domestic crypto platforms. Retail users can execute transfers and interact with crypto indirectly, yet larger or repetitive transactions often trigger compliance reviews or require documentation on sources of funds. While day-to-day operations are feasible, volatility in policy and FX controls means that users must plan their transfers carefully.

In contrast, Colombia approaches crypto access through sandbox-backed pilots and more structured fintech oversight.

Colombia: Sandbox-Driven Crypto Access

Colombia follows a controlled, pilot-based approach to crypto-related banking, relying on regulatory sandboxes rather than broad market adoption. Instead of allowing open crypto access across the banking system, regulators supervise limited experiments with licensed exchanges and selected financial institutions [5].

In operational terms, crypto access in Colombia is shaped by permissioned participation rather than general tolerance. Transactions linked to sandbox-approved partners and predefined use cases tend to process smoothly within set limits. Activity outside these pilots – or volumes that exceed approved thresholds – typically triggers manual compliance reviews or is restricted altogether. Predictability depends less on user behavior and more on whether the transaction falls within an active regulatory program.

Bancolombia [12] is one of the few major banks participating in these sandbox initiatives, working with approved crypto exchanges under regulator supervision.

For users operating within these frameworks, basic crypto-fiat flows are feasible. However, the scope remains narrow, volumes are capped, and continuity beyond pilot phases is not guaranteed.

For users operating within these frameworks, basic crypto-fiat flows are feasible. However, the scope remains narrow, volumes are capped, and continuity beyond pilot phases is not guaranteed.

Proceeding south, Panama adopts a divergent strategy: although the nation provides dollarized accounts and banking flexibility, regulatory transparency is less robust, necessitating users to exercise vigilance about documentation and adopt prudent transaction procedures.

Panama: Flexible but Cautious

Panama combines a dollarized economy with relatively flexible banking access, but regulatory guidance on cryptocurrency remains limited and fragmented [6]. While crypto-related activity is not explicitly prohibited, banks rely heavily on internal compliance frameworks rather than clear, unified regulatory rules.

In operational terms, crypto banking in Panama depends on documentation quality and onboarding depth rather than transaction routing. Banks are generally open to crypto-linked activity once clients pass enhanced due diligence, but larger or atypical transfers frequently shift accounts into manual compliance review. Predictability improves significantly after onboarding, yet flexibility declines as volumes or transaction patterns change.

Banco General [18] offers multi-currency accounts, regional transfer capabilities, and robust online banking tools that support everyday operations. Crypto-related transfers are feasible, though higher-value or unusual activity is commonly subject to manual verification.

Towerbank [13], often cited for its crypto-tolerant positioning, provides USD rails and interfaces for registered crypto-related transactions. Once onboarding requirements are met, transfers tend to process more smoothly, although documentation standards remain strict.

Towerbank [13], often cited for its crypto-tolerant positioning, provides USD rails and interfaces for registered crypto-related transactions. Once onboarding requirements are met, transfers tend to process more smoothly, although documentation standards remain strict.

For users operating within these constraints, Panama offers workable crypto-fiat access. However, success relies on precise paperwork, stable transaction patterns, and readiness for manual compliance checks.

Banks in Latin America rarely ban crypto outright. More often, users run into tighter AML checks, manual compliance reviews, or sudden changes in limits and internal policies as regulators tighten oversight [4][14]. In practice, stable operation in the region comes from a defensive, compliance-first approach: spreading activity across multiple accounts, keeping clean records for every transfer, starting with small amounts, and adjusting flows to local regulatory and FX rules. Relying on a single “crypto-friendly” bank is usually not enough.

With the country-level picture established, the next step is to understand what truly drives bank behavior in practice: regulation, internal risk models, and compliance execution rather than advertised “crypto-friendly” positioning.

What Really Matters: Regulation, Reliability, Transparency

In Latin America, the difference between a truly reliable “crypto-friendly” bank and a risky one rarely comes down to visible features or marketing claims. In practice, it is shaped by regulatory structure, internal risk models, and how each bank applies compliance rules on a day-to-day basis.

What you must verify

Before choosing a bank, the real questions are simple:

- What actually signals that a bank can handle crypto activity consistently, without sudden freezes or reversals?

- Why do banks offering similar services behave so differently once crypto-related transactions begin?

The answer usually lies beyond product features.

Why do banks behave so differently?

Latin America operates without a unified framework for cryptocurrencies. Each country follows its own regulatory logic, leaving banks with wide discretion over risk management.

Brazil enforces strict AML oversight through its central bank and securities regulators. Mexico routes crypto access through licensed platforms while banks remain conservative by default. Argentina blends widespread crypto usage with FX controls and abrupt policy shifts. Colombia limits exposure through supervised sandbox programs, while Panama offers flexibility via dollarized banking but provides little formal crypto guidance.

Because of this fragmentation, banks rely less on public crypto policies and more on internal risk scoring, transaction pattern analysis, and manual compliance reviews. What looks acceptable one month may trigger scrutiny the next.

Signals that actually matter

In Latin America, reliable crypto-friendly behavior is usually tied to a small set of practical signals rather than public statements or feature lists:

- A proven track record of processing transfers to regulated exchanges or licensed fintech partners.

- Stable performance as transaction volumes grow, not just at entry-level amounts.

- Clear and responsive communication from compliance teams during reviews.

- Established banking infrastructure with a long operational history.

- Consistency over time, rather than temporary tolerance during pilots or market hype cycles.

A bank’s stance can change quickly – not because crypto becomes illegal, but due to shifts in internal risk thresholds, fraud alerts, or regulatory pressure. This is where theory meets practice. While banks may appear crypto-friendly on paper, real user experience often exposes hidden rules, internal triggers, and uneven compliance handling.

The following section draws on verified user discussions from 2024–2026 to illustrate how these dynamics play out in practice [15].

Real User Reviews (2024–2026): What Actually Happens in Practice

Public policies and feature lists rarely reflect how banks behave once real money and real crypto are involved. A clearer picture emerges from user discussions on Reddit and X between 2024 and early 2026, which highlight recurring operational patterns rather than isolated incidents across Latin America [15].

Nubank (Brazil)

Users who purchase Bitcoin through Nubank often discover that the bank retains custody of the assets, meaning customers do not directly control private keys. In multiple discussions, users question whether funds could be restricted, delayed, or limited under Nubank’s internal rules – particularly during compliance reviews or policy updates. While daily usability is generally praised, concerns around ownership and control tend to surface when conditions change [15].

Similar doubts appear across Brazilian crypto communities, where users debate how withdrawals and asset custody actually function within the app, based on recurring discussions on Reddit.

BBVA Mexico (Mexico)

In Mexican forums, users frequently note that BBVA’s behavior varies depending on how crypto exposure is structured. Transfers routed through licensed platforms such as Bitso tend to process more smoothly, while direct transfers to certain exchanges may be delayed or reviewed. These patterns reinforce the perception that BBVA prefers regulated intermediaries and applies stricter checks when crypto activity appears direct or unfamiliar [19].

Banco General (Panama)

Discussions around Banco General focus less on outright blocks and more on how crypto-related transactions are classified. Users report that crypto purchases made with Banco General cards may be treated as quasi-cash, sometimes resulting in additional fees or manual review. While general online banking reliability is viewed positively, larger or atypical crypto-linked transactions often attract closer scrutiny [20].

Among Panama-based users, Towerbank is frequently mentioned as a more predictable option for crypto-related activity, particularly for business clients. Community members describe fewer interruptions once onboarding is completed, although strict documentation requirements at the start are consistently noted. The trade-off – predictability over convenience – is often seen as acceptable by users prioritizing operational stability [21].

What these experiences show

Taken together, these discussions point to a consistent reality: in Latin America, crypto banking usually works – but not automatically and not without limits. Banks rarely ban crypto outright. Instead, friction tends to emerge as volumes increase, transaction patterns change, or custodial exposure grows. Real-world behavior, not advertised features, ultimately determines how reliable a banking setup remains over time.

Opportunities vs. Risks

Choosing a bank for crypto operations in Latin America is always a trade-off. Some users move funds with minimal friction, while others encounter delays, reviews, or sudden limits. In most cases, the difference comes down to expectations: those who understand both the upside and the constraints tend to operate far more smoothly.

The graph above visualizes the balance of Opportunities vs. Risks when choosing a crypto-friendly bank in Latin America. As shown, some banks provide smooth operations with minimal friction, especially when using reliable fiat rails into crypto (often via licensed fintech partners). However, in some cases, delays, reviews, and sudden limits can cause operational challenges.

Opportunities

When conditions align, crypto-friendly banks in the region can offer:

- Reliable fiat rails into crypto, especially when transfers are routed through licensed fintech partners.

- Multi-currency accounts that support cross-border activity and regional diversification.

- Access to stablecoins, typically via exchanges or partner platforms rather than directly.

- Low friction for small to mid-sized transfers that match a typical user profile.

- Regulated custody or brokerage services for institutional or high-net-worth clients.

For many users, these capabilities are sufficient to build a functional crypto–fiat setup – as long as volumes and frequency remain controlled.

Risks

At the same time, recurring user reports point to several structural risks:

- Temporary account suspensions caused by unclear or shifting transaction patterns.

- Lengthy compliance reviews, particularly after volume increases.

- Sudden policy changes at the bank or regulatory level.

- Strict limits on large deposits or withdrawals.

- Country-specific constraints, including FX controls or partial restrictions.

Opportunities across the region are real and gradually expanding. But so are the constraints. Understanding both sides clearly makes it easier to plan next steps, adjust behavior early, and avoid unnecessary surprises.

How to Choose the Right Bank: A Practical Framework

In Latin America, choosing a bank for crypto activity is rarely about finding the “best” option. It is about reducing uncertainty. Assumptions and marketing promises break down quickly once real transactions begin, so the only workable approach is a step-by-step reality check.

The process

- Start with geography. Regulations, limits, and enforcement vary sharply by country, so only consider banks and fintechs that operate locally and are actively used by residents.

- Next, look past feature lists. What matters is not whether a bank claims to be crypto-friendly, but how transfers behave in real conditions. This includes how often reviews occur, what triggers additional checks, and whether outbound transactions are treated consistently.

- Recent user experience is critical. Discussions and reports from 2024–2026 often reveal patterns that official documentation does not, especially around freezes, delays, or changing internal thresholds.

- Before committing meaningful funds, review the practical constraints. Fees, transfer limits, and AML requirements tend to matter most on the way out, not on the initial deposit.

- Open the account and test it with a small amount. Most structural issues surface early, when volumes are low and the cost of adjustment is minimal.

Only after this should activity scale, ideally spread across more than one institution to avoid single-point failure.

When this process is followed, problems tend to appear sooner rather than later, giving users time to adapt before risk becomes material.

Where Banks End, Crypto Infrastructure Begins (Why Non-Custodial Tools Matter)

Even the most crypto-friendly banks stop at fiat rails. They do not execute on-chain swaps or provide full self-custody. This gap is where operational friction often starts.

To reduce it, many users rely on non-custodial conversion layers that sit between banks and blockchains.

For example, ChangeNOW enables fiat-to-crypto and crypto-to-fiat conversions without holding user funds, which helps avoid custodial risk and reduces common AML triggers linked to asset storage. Because funds remain non-custodial during the swap, banks often treat these transactions more like verified transfers than high-risk wallet custody. A standard, one-time verification process helps maintain compliance while preserving flexibility.

Before opening an account, ask yourself: Have I covered all safety points? This checklist gives a quick way to verify readiness.

Pre-Flight Checklist

Before committing to a setup, a quick checklist helps catch weak points:

- Regulation: Is the bank licensed and insured?

- Reviews: Are there recent reports of freezes or blocked transfers?

- Crypto access: Which assets and transfer paths are supported?

- Limits: What are the real deposit and withdrawal ceilings?

- Support: How responsive is customer service during reviews?

- Flexibility: Are multi-currency accounts or stablecoins available?

If each box is reasonably covered, the likelihood of operational issues drops sharply.

What to Do Next

Once the groundwork is done, action becomes straightforward:

- Define your jurisdiction and risk tolerance

- Select from a short list of proven banks or fintechs

- Cross-check recent user feedback

- Compare compliance thresholds and fees

- Run a controlled test transaction

- Diversify – combine bank accounts with crypto-native tools

This approach reduces uncertainty and supports long-term stability.

Future Outlook for 2026

In 2026, crypto-friendly banking is no longer moving in an experimental direction. The market has shifted toward more structured, compliance-driven integration, with fewer grey zones and less tolerance for ambiguous activity.

What defines 2026

- Deeper crypto integration inside neobanks, primarily through partnerships rather than native custody.

- Improved stablecoin payment support, especially for cross-border settlements and treasury operations.

- More consistent AML enforcement, driven by refined internal risk models and transaction analytics.

- Fewer arbitrary account freezes, as banks increasingly rely on behavioral patterns instead of blunt volume thresholds.

- Clearer regulatory positioning, even in regions without unified crypto frameworks.

In practice, this means banks in 2026 are less reactive and more rule-based. Crypto activity is neither ignored nor treated as exceptional – it is assessed through standardized compliance logic.

What this means for users

Users operating in 2026 benefit most when they adopt a structured setup:

- diversified across banks and fintechs,

- aligned with local regulatory expectations,

- supported by clear transaction histories and documentation.

The era of “trial-and-error” crypto banking is largely over. In 2026, smoother operations favor those who treat crypto not as an exception but as a regular financial activity governed by predictable rules.

Final Conclusion

In 2026, crypto-friendly banking offers more usable options – but only for users who approach it strategically. The idea of a single “perfect” bank is outdated. What works in practice is a diversified setup, shaped by local regulations, realistic transaction behavior, and a clear separation between banking and crypto infrastructure.

Effective strategies in 2026 are built around jurisdiction-aware bank selection, gradual scaling, and the use of non-custodial tools as a buffer between fiat rails and on-chain activity. This structure reduces AML friction, limits exposure to sudden policy shifts, and improves operational stability.

For experienced users, a hybrid model is now standard: banks provide fiat access and compliance, while crypto-native services handle conversions and blockchain interaction. This balance delivers flexibility without sacrificing control.

Bank policies continue to evolve, and geography remains the decisive factor. The most resilient setups in 2026 are those based on diversification, documentation, and predictable transaction patterns. Confidence in crypto banking no longer comes from a single account but from a well-designed, adaptable system.

Reader’s Roadmap

This guide is well structured to help each reader type move efficiently through the material:

For Latin America: Start with the Regional Analysis, then review the Bank Matrix and Real User Reviews. Finish with the Step-by-Step Framework and Checklist.

For higher-risk jurisdictions: Focus on Risks vs. Opportunities and Regulation & Reliability before opening or scaling accounts.

For newcomers:

Begin with regulatory fundamentals, follow the framework, and validate your setup with the checklist.

Resources

- Central Bank of Brazil – PIX & instant payment system (official framework)

- Banco Central do Brasil – Drex (CBDC pilot)

- Mexico Fintech Law & crypto intermediaries (CNBV overview)

- Central Bank of Argentina (BCRA) – FX controls & crypto regulatory stance

- Superintendencia Financiera de Colombia – crypto sandbox program (La Arenera)

- Panama banking & crypto regulatory overview (Superintendencia de Bancos de Panamá)

- Nubank – official website

- Banco Inter – crypto-related investment products

- BTG Pactual – institutional banking & crypto services

- Bitso – regulatory positioning & SPEI integration

- BBVA Mexico)

- Bancolombia – participation in crypto sandbox pilots

- Towerbank – crypto-friendly banking positioning

- D&A CryptoMap – regional crypto regulation overview

- Aggregated user reviews and community discussions (2024–2026)

- Santander Argentina – official website

- Banco Galicia – official website

- Banco General – official website

- Reddit (Mexico) – exchange alternatives / Bitso context discussion

- Reddit (Panama) – buying crypto with Banco General VISA

- Reddit (Panama) – experiences with Towerbank / Metrobank

- ChangeNOW – Buy crypto